Europe's accounting tech is fragmented. Breakdown country by country!

Europe isn't one accounting market. It's twenty seven (plus UK, Norway, etc) very different ones, each with its own software champion, its own role for accountants, and its own pace of digital reform. For our State of European Accounting Tech 2026 report, we surveyed 1,400 SMEs (3 to 200 employees) across ten countries. They cited more than 150 distinct accounting solutions. That single number tells you most of the story.

Europe isn't one market, it's a collection of local ones

There's no single accounting "operating system" in Europe. Unlike the US, the landscape is shaped country by country, by national tax rules, professional standards, and local distribution channels.

The numbers back this up. Across the ten countries we surveyed, 54% of companies manage accounting internally, 20% fully outsource it to an external accountant, and 27% run a hybrid model that combines internal ownership with external validation. Smaller companies are far more likely to outsource. Larger SMEs tend to keep finance in-house while keeping an accountant for oversight.

Even the big international vendors play a local game. Sage, Wolters Kluwer, TeamSystem, and Visma all operate through localized products, often built through acquisitions and shaped by country-specific compliance rules. Truly global platforms like Xero, NetSuite, and Odoo show up across multiple markets, but they're the exception in a landscape still dominated by domestic tools.

The practical takeaway: software usage is multi-stack, not single-tool. Most companies run several systems at once, pairing a core accounting tool with complementary software depending on their workflows.

Two ways to read every market: accountant tools vs SME tools

To make sense of any European market, you need to split accounting software into two categories.

Tools built for accountants are designed around the firm's workflow: managing many client portfolios, producing compliance, filing tax, and preparing statutory accounts. Tools built for SMEs are used directly by companies managing their own books, from lightweight cloud invoicing apps to full ERP systems. A growing group of platforms serve both at once, giving the SME and its accountant a shared view of the same data.

Which category a tool belongs to decides how you integrate with it, how it's distributed, and how you prioritize it. Reaching the accountant channel demands a completely different go-to-market than selling directly to SMEs. And in accountant-centric markets, France, Italy, Spain, and Belgium, the accountant channel is effectively the only viable path to scale. A tool that doesn't fit the accountant's workflow faces a structural barrier to adoption, no matter how good it is.

The country-by-country map

Here's how the ten markets break down: who owns the workflow, which tools dominate, and where e-invoicing rules stand.

🇫🇷 France: accountant-led, with cloud challengers rising

France has 5.2 million SMEs and one of Europe's most regulated accounting professions. Experts-comptables hold legal authority over statutory reporting and tax, and close to 80% of very small companies outsource accounting entirely to them. The legacy accountant suites are Cegid Quadra and Sage Génération Expert, with Fulll and Cegid Loop as the cloud challengers. Pennylane and Tiime bridge SMEs and accountants on shared data, and Pennylane has grown fast since 2020. B2B e-invoicing becomes mandatory from September 2026.

🇩🇪 Germany: the most accountant-driven market in Europe

Germany has 3.1 million SMEs, and for most of them, accounting is fully delegated to a Steuerberater (tax advisor) who often handles payroll too. The SME rarely touches the production system, so the accountant decides the software. DATEV sits at the centre of the market, with a 47% survey share that almost certainly understates its real footprint. Lexware Office and Sevdesk serve SMEs more directly. Businesses have had to receive structured e-invoices since January 2025, with issuing mandatory from 2027 for companies above €800,000 turnover and from 2028 for everyone else.

🇬🇧 United Kingdom: competitive, cloud-first, advisor-led

The UK has 5.5 million SMEs and the most competitive market in our panel, with the highest multi-tool adoption rate: 89 of 200 UK respondents use two or more tools at once. Xero, QuickBooks, and FreeAgent dominate the SME and accountant-facing layer, all built around accountant-client co-usage. Sage spans three products (Sage 50, Sage 200, Sage Intacct) across company sizes. UK accountants act as strategic advisors who help clients choose and run their own software, rather than taking the books over entirely. A Peppol-based e-invoicing mandate is planned for 2029.

🇪🇸 Spain: the asesoría runs the show

Spain has 2.9 million SMEs and around 150,000 small advisory and accounting practices (asesorías). Roughly 80% of Spanish SMEs outsource bookkeeping and tax filing, and many never see the software at all. The accountant-grade market is dominated by Wolters Kluwer's A3 suite and the Sage ecosystem. Tech-savvy entrepreneurs sometimes use lighter tools like Holded directly. Two reforms are reshaping the market: Veri*Factu (certified invoicing software) from 2027, and the Crea y Crece B2B e-invoicing mandate, expected for large companies in late 2027 and everyone else through 2028.

🇮🇹 Italy: the e-invoicing pioneer, locked around the commercialista

Italy has 4.2 million SMEs and was the EU pioneer on e-invoicing: mandatory B2B since 2019 through the government's SDI platform. It also has the lowest multi-software rate of any country we surveyed, just 19%, reflecting how much accounting stays a single-system, accountant-managed workflow. The market is organized around three families: TeamSystem (Studio, Azienda, Gamma, Alyante), Zucchetti (AGO Infinity), and Wolters Kluwer (B.Point and the cloud-native Genya).

🇧🇪 Belgium: one country, two sub-markets

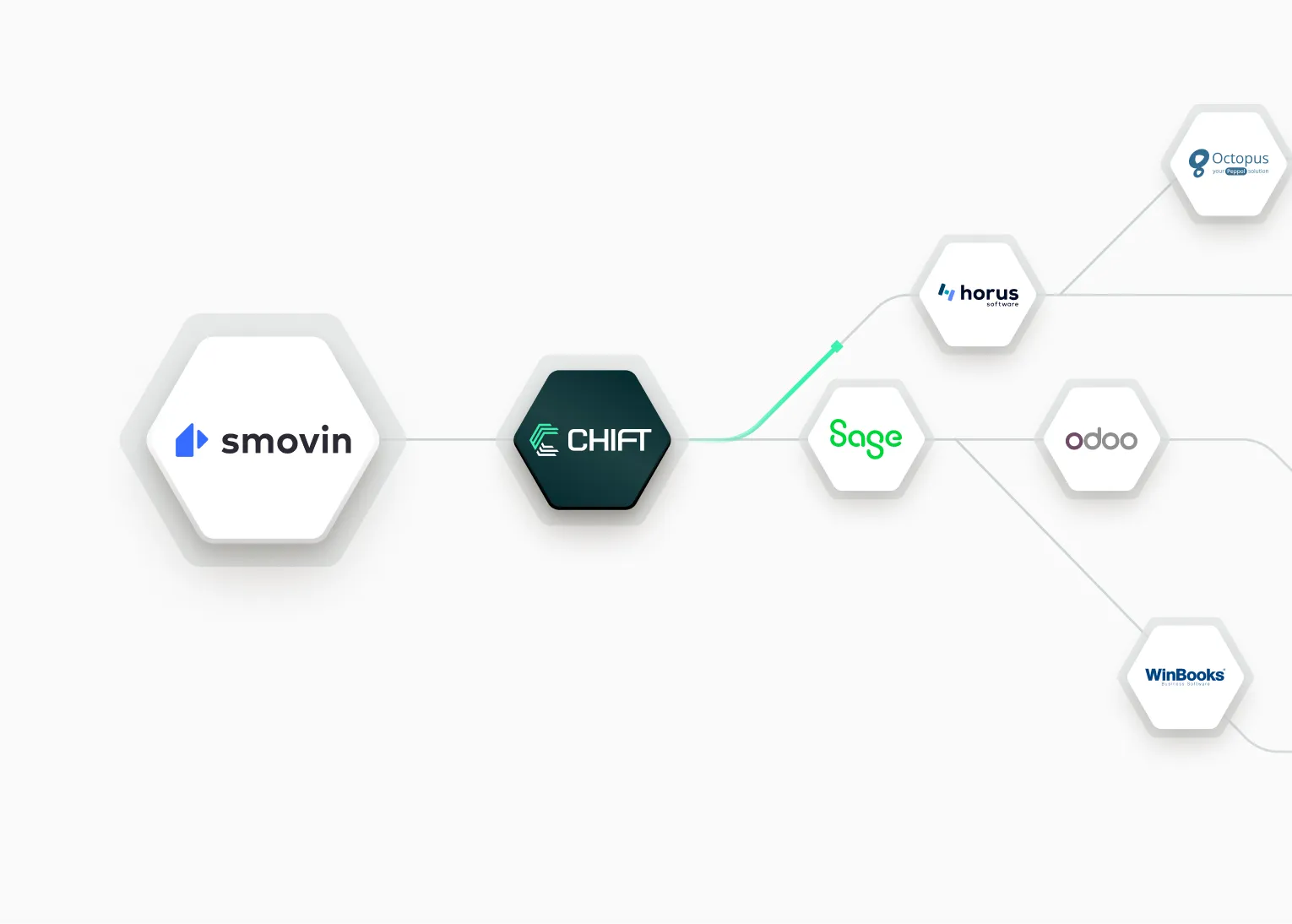

Belgium became one of Europe's most advanced e-invoicing markets when structured B2B e-invoicing via Peppol became mandatory on 1 January 2026. Chartered accountants run the full workflow for most SMEs, and for companies below 50 employees, accounting is almost entirely outsourced. The market splits cleanly by region. Flanders is cloud-first and collaborative (Exact Online, Octopus, Yuki, Adsolut), while Wallonia stays more on-premise and integrator-managed (Winbooks, Sage BOB50, Horus, Odoo). A vendor entering Belgium is really entering two distinct markets.

🇳🇱 Netherlands: digitally advanced and best-of-breed

The Netherlands has 1.5 million SMEs and is one of Europe's most digitally mature markets. Dutch entrepreneurs often start without an accountant and bring one in later, mainly for compliance and annual accounts, so accountants act as compliance partners more than day-one advisors. Exact Online and AFAS anchor the market, followed by a long tail of SME tools (e-boekhouden, Moneybird) and accountant software (Twinfield, Yuki, Visma AccountView). A strong best-of-breed culture means companies combine separate tools for accounting, invoicing, expenses, and payroll, which makes connectivity a practical necessity. B2B e-invoicing is not mandatory.

🇸🇪 Sweden: consolidated, collaborative, Fortnox-centred

Sweden has 1.2 million SMEs and a market where the line between SME tools and accountant tools has largely dissolved. Fortnox is the clear leader, present in 80% or more of firms with five or more employees, and built around shared access between SMEs and their accountants. Visma Spiris (formerly Ekonomi) is the second major platform. SMEs typically handle day-to-day bookkeeping themselves and rely on an accountant for compliance and year-end. PE-backed consolidation is increasingly moving software decisions to group level. B2B e-invoicing is not yet mandatory.

🇩🇰 Denmark: regulation made digital the default

Denmark has 300,000 SMEs and a market shaped by law: the Bookkeeping Act effectively ends manual ledgers and spreadsheets for official accounting, making certified digital bookkeeping the default. Visma e-conomic is the undisputed leader, serving SMEs and accountants in one environment, followed by Dinero, Uniconta, and Billy by Ageras. Over 100 bookkeeping systems are officially registered with the Danish Business Authority, and that certification requirement is a real barrier to entry for any new vendor. Denmark's hybrid model is dominant: SMEs handle daily bookkeeping, accountants handle compliance.

🇳🇴 Norway: collaborative platforms and early e-invoicing

Norway has 600,000 SMEs and a strongly collaborative model where SMEs and accountants work inside the same tools, primarily Tripletex, Fiken, and PowerOffice. The country is one of Europe's most advanced on e-invoicing infrastructure, with roughly half of all B2B and B2G invoices already exchanged electronically via Peppol. That maturity pushed the government to accelerate its mandate: structured e-invoice issuance becomes mandatory for businesses with bookkeeping obligations from 1 January 2027.

{{CTA-1}}

The regulation wave makes connectivity strategic

Across Europe, mandatory e-invoicing and digital bookkeeping reforms are arriving on overlapping timelines: Italy since 2019, Belgium from January 2026, France from September 2026, Norway and Germany from 2027, Spain through 2027 and 2028, and the UK in 2029.

These reforms do more than change an invoice format. They push SMEs toward compliant tooling and increase multi-software adoption, since companies often pair their accounting platform with a separate compliance or invoicing layer. The more tools in the stack, the more data has to move between them. That's why integrations are becoming core infrastructure rather than a nice-to-have, and why connectivity is now a strategic decision, not a technical detail.

What this means for software vendors

Expanding across Europe takes more than translating your interface. It takes a market-by-market approach: an understanding of how accounting actually works in each country, who decides which software gets adopted, and the ability to connect with a wide range of country-specific tools.

The prize is growing fast. As one expert puts it in our report, accounting software in Europe is roughly a €6 billion market, while accounting services are close to €100 billion. As automation lets fewer accountants serve more clients, value is steadily shifting from services to software, blurring the line between the two and expanding the opportunity by an order of magnitude.

For SaaS vendors and fintechs, that shift is only capturable if your product can plug into the financial tools your customers already use. In a fragmented market, the integration layer is the difference between entering one country and entering ten.

Which of these tools does Chift already connect to?

Knowing the map is one thing. Connecting to it is another. Here's where Chift's live accounting coverage stands today, against the tools that dominate each market. One integration to Chift activates any of them in a click.

🇫🇷 France: Pennylane, Acd, Cegid Loop, Fulll, MyUnisoft, Sage Génération Experts, Sage 100 FR, Sage 50 FR, and Tiime. That covers both the accountant suites and the cloud platforms bridging SMEs and their experts-comptables.

🇩🇪 Germany: DATEV, the backbone of the German market, plus Sevdesk by Cegid for the cloud SME segment and Business Central for the mid-market.

🇬🇧 United Kingdom: Xero, QuickBooks, FreeAgent, Sage Intacct, and Business Central. The collaborative top tier of the UK market, covered.

🇪🇸 Spain: a3ERP and Sage 200 ES for the asesoría channel, Holded for tech-savvy SMEs, and Odoo, Oracle NetSuite, and Business Central for companies scaling up.

🇮🇹 Italy: TeamSystem Reviso from the dominant TeamSystem family, alongside Business Central and Oracle NetSuite for SMEs moving to ERP.

🇧🇪 Belgium: full coverage of both sub-markets. Exact, Octopus, and Yuki for cloud-first Flanders, plus WinBooks, Sage BOB50, Horus, and Odoo for Wallonia.

🇳🇱 Netherlands: Exact, AFAS, Twinfield, Yuki, e-Boekhouden.nl, Moneybird, Minox, and SnelStart. Deep coverage for one of Europe's most best-of-breed markets.

🇸🇪🇩🇰🇳🇴 The Nordics: Tripletex and Fiken in Norway, plus Visma Spiris and Visma eAccounting in Sweden, with Nordic coverage growing across the region.

We build and release new connectors every month, so this list keeps growing. You can see the full live coverage on our integrations page.

Want the full data? Download the complete State of European Accounting Tech 2026 report.

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.webp)

.webp)

.jpg)

.jpg)

.webp)

.jpg)

.webp)

.avif)