If you run a neobank or fintech, you've probably encountered the issue of automatically getting transactions into accounting software. There are two potential options to this. One is joining an Open Banking provider. The other is building direct integrations with accounting software, both are valid, and they're built for different things.

What does an Open Banking provider do?

Open Banking providers are unified APIs for banks. They aggregate banking data from dozens of financial institutions and expose it through a single API. Accounting software can then retrieve banking transactions from all their connected banks via that one integration.

Here's how it works for you as a neobank: you become a connector in their network. Clients of the Open Banking provider pull data from you specifically, transaction-level data such as amounts, dates, transaction descriptions, counterparty IBANs, and basic account balances. You're listed in their catalogue, and when a user wants to connect their bank account, they authenticate through the provider's flow. That data then flows into whichever accounting tool the provider supports, typically as a bank statement feed ready for reconciliation.

This model is well-established and widely used. It's a straightforward way to get your transactions visible inside accounting tools that have already built on top of these providers.

What does integrating with Chift look like?

Instead of being limited to a basic transaction feed, you integrate once with Chift's unified API and unlock access to the full accounting data model across 100+ connectors in Europe.

More data. More use cases. One integration.

Where Open Banking stops at amounts, dates, and IBANs, Chift lets you send enriched transaction data, retrieve invoices and expenses, pre-match payments against open receivables, and power use cases like lending or spend management all through the same connection.

How the two approaches compare on bank feed data

Open Banking integrations typically cover the core transaction feed: amount, date, description, and IBAN. That's enough for basic reconciliation in most modern accounting tools.

Chift supports two integration routes for bank feeds, giving you more flexibility depending on the target software:

financial_entries, which posts transactions directly as accounting journal entries. This works well for legacy accounting software, where each bank transaction becomes one accounting entry.bank_transactions, which imports transactions as bank statement lines into ERPs like NetSuite, Odoo, or Exact Online. This enables automatic reconciliation flows inside the ERP, with a smoother user experience for the end user.

Because you're actively pushing data through Chift, you're not constrained by what the protocol exposes. Metadata that lives in your platform analytical dimensions, custom categorisation, enriched counterparty data can travel with the transaction into the accounting software. Chift also supports cash transaction synchronization, something Open Banking cannot cover at all since it's inherently scoped to bank accounts.

On top of that, data sent through Chift can be enriched before it reaches the accounting software: counterparty assignment, bank fee detection, pre-matching against open invoices. This turns a transaction feed into a pre-accounting automation layer.

Coverage: where each approach reaches

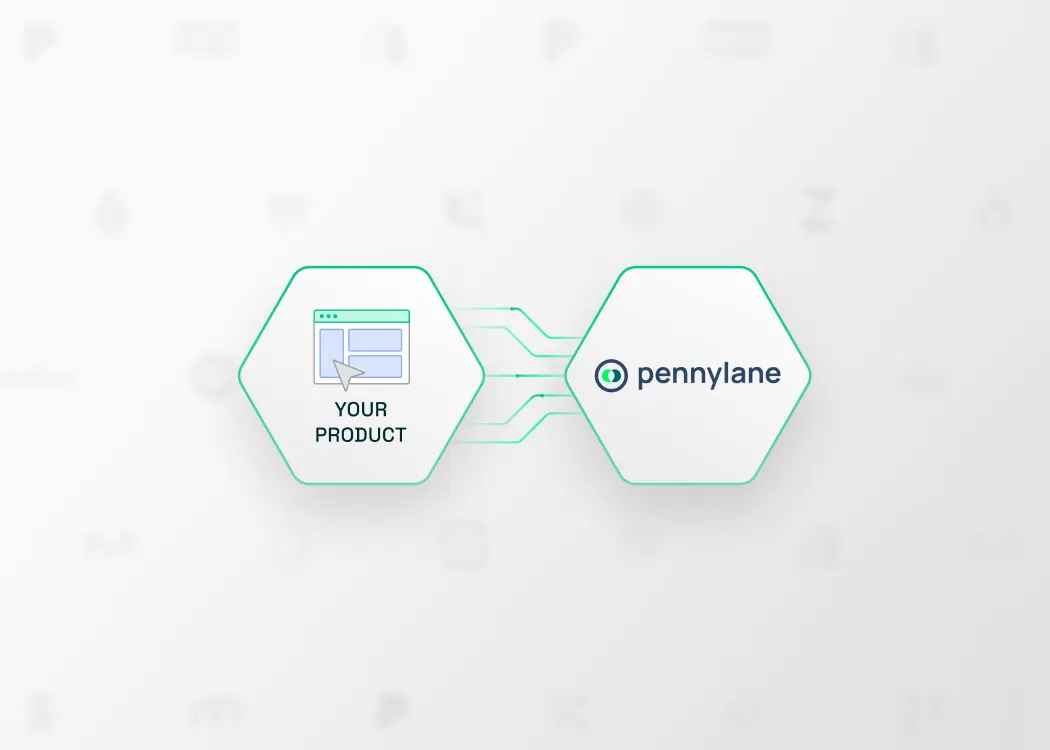

Open Banking via PSD2 covers a broad range of banks and connects well to modern accounting tools that have built on these networks. If your target market is primarily using tools like Pennylane, Xero, or other platforms with native Open Banking support, it's a solid path.

Chift's coverage extends further into legacy and local European systems that sit outside Open Banking networks. DATEV in Germany, Winbooks in Belgium, Cegid Loop in France, Sage Intacct, MS Dynamics: these connectors are live on Chift and are accessible through our unified API. For neobanks with customers across multiple European markets using a wide variety of tools, this breadth matters.

Revolut, Wise, IbanFirst, and Qonto all chose Chift to complement or replace direct Open Banking integrations, specifically because Chift reaches accounting software their customers were actually using.

Beyond bank feeds: what Chift unlocks additionally

This is where the two approaches diverge most clearly.

Open Banking providers are built for one thing: getting bank transactions into accounting tools. That's exactly what they do, and they do it well.

But most neobanks don't stop at payments. Invoicing modules, expense management, lending. Chift's unified API covers the full accounting object model, which means once you're integrated, you can activate additional use cases that go well beyond transaction feeds.

Invoice and expense management. Retrieve invoices or expenses from your customers' accounting software. Push spend data from your app back into their books. If you have a card product or an expense workflow, this closes the loop between your product and your customers' accounting.

Accounts payable and receivable. Access open invoices to pre-match them with incoming payments, reducing manual reconciliation significantly.

Lending and credit assessment. With access to a company's accounting data through Chift, you can analyse their financial health in real time, reviewing receivables, payables, cash position, and historical trends to support faster, more informed credit decisions.

These use cases aren't available through Open Banking providers. They require deeper access to the accounting data model, which is what Chift provides.

Choosing the right path for your product

Open Banking is a great fit if your goal is to appear as a trusted bank in a short list of modern accounting tools with minimal setup. It's low-friction and cost-effective for that specific scope.

Chift makes more sense when you want to own the integration experience, reach a broader range of European accounting software, send richer transaction data, or build towards higher-value use cases like lending or spend management as your product grows.

Some neobanks use both. Others start with Open Banking and expand to Chift when their customers' needs outgrow what a basic bank feed covers.

Why choose Chift

- Active integrations with 100+ accounting and ERP connectors across Europe

- Two bank feed routes: direct accounting entries and bank statement lines

- Pre-accounting enrichment: counterparty assignment, fee detection, invoice pre-matching

- Coverage of legacy and local systems beyond the Open Banking network

- Unlocks invoicing, lending, expense, and spend management use cases

- One integration, maintained by Chift, so your engineering team can stay focused

Revolut, Qonto, Wise, and IbanFirst chose Chift to scale bank feed integrations across Europe. Read the Qonto case study to see how it works in practice.

Want to explore what Chift could add to your integration strategy? Talk to our team.

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.webp)

.webp)

.jpg)

.jpg)

.webp)

.jpg)

.webp)

.avif)