France's forthcoming e-invoicing reform extends beyond the digitalization of invoices.

The regulatory framework rests on two complementary pillars:

- E-invoicing, governing domestic B2B transactions

- E-reporting, for all transactions not covered by e-invoicing.

In short, e-reporting applies to any sales that does not generate a mandatory electronic invoice, yet still needs to be reported electronically to the French Tax Authority (DGFiP).

This is where POS systems assume an essential role.

The mirror of e-invoicing

E-reporting requires businesses to electronically transmit transaction data about:

- B2C sales in France

- International B2B sales, within or outside the EU.

The aim is to give the tax authority a real-time view of business activity, simplify VAT pre-filling, and strengthen anti-fraud controls.

This obligation applies to everyone, from large corporations to small retailers and micro-businesses. Even traditional cash registers are covered.

A phased rollout

E-reporting will follow the same implementation schedule as e-invoicing:

- September 1, 2026 → Large enterprises and mid-sized companies,

- September 1, 2027 → SMEs, micro-businesses, and freelancers.

Every business will need to digitally transmit sales data to remain compliant.

Two types of reporting

The e-reporting framework encompasses two distinct declaration streams:

- Transaction reporting, covering B2C and international B2B

- Payment reporting, applicable to service providers operating under cash-basis VAT.

Submission frequency is determined by the entity's VAT, every 10 days, monthly, or quarterly.

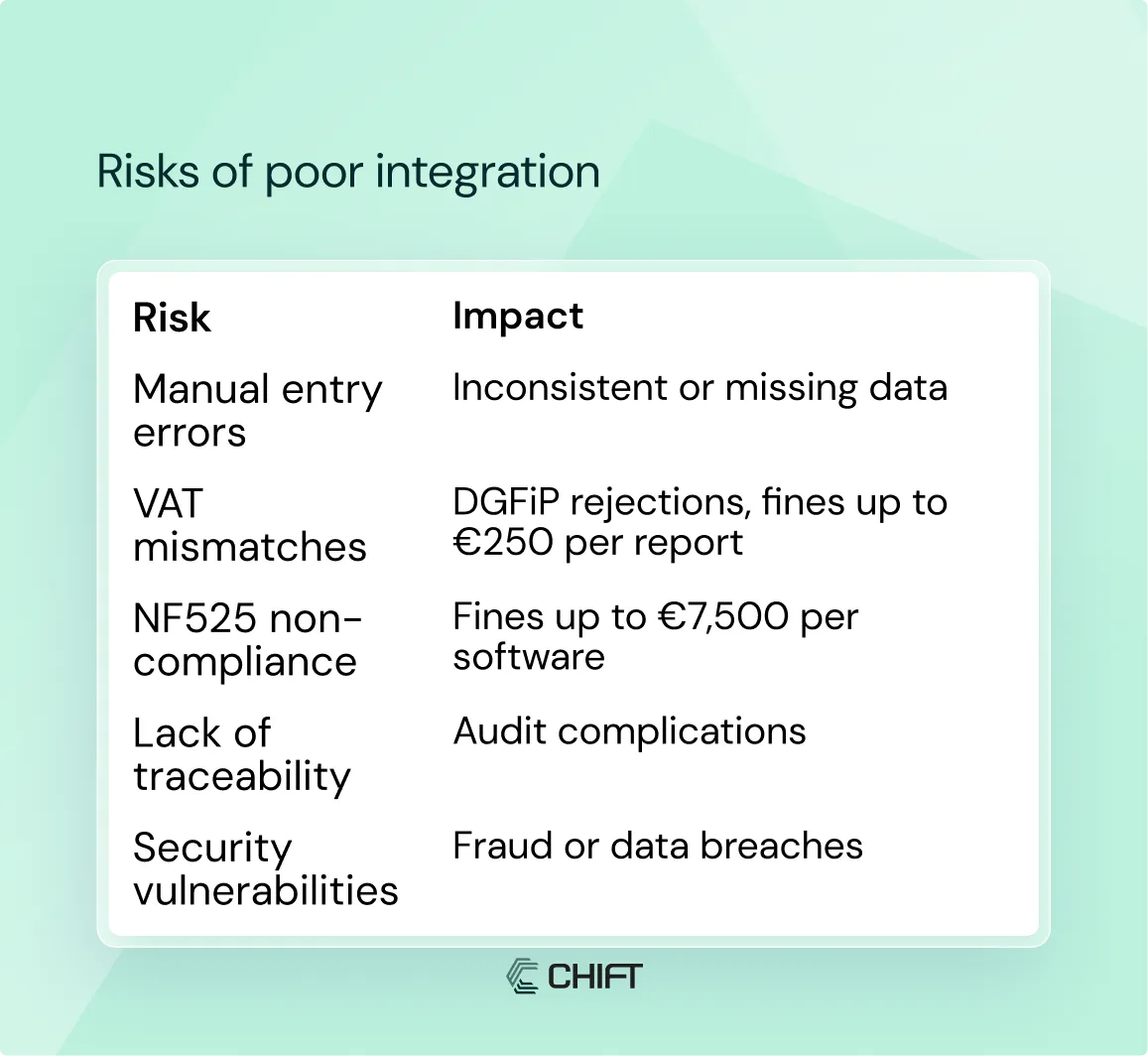

The practical challenge for POS systems

A typical POS system processes hundreds transaction lines monthly across multiple locations, channels. Manual data entry at this scale is operationally unfeasible.

Businesses must therefore establish capabilities to:

- Automate data extraction from POS systems

- Ensure consistency with accounting records

- Secure and trace data flows

- Stay compliant with DGFiP and AFNOR standards.

Integration at the heart of compliance

E-reporting compliance is fundamentally dependent on interconnected systems.

The key layers are involved

- POS systems, capturing transactions and payments,

- Accounting / ERP systems, consolidating data,

- Partner Platforms (PA), transmitting information to the Public Invoicing Portal (PPF).

Two main models exist:

- Full integration (POS → Accounting → Partner Platform → DGFiP)

- → Ensures consistency and full traceability.

- Simplified flow (POS → Partner Platform → DGFiP)

- → Easier for small businesses, but higher risk of misalignment with accounting.

The risks of poor integration

The path toward intelligent automation

Effective preparation for e-reporting means connecting systems and automating data flows:

- Building API connections between POS and accounting,

- Using certified Partner Platforms,

- Setting up real-time monitoring and alerts,

- Synchronizing data continuously,

- Keeping a complete audit trail.

This is precisely where Chift delivers strategic value: a unified POS API connecting leading cash register systems to accounting and tax software through a single integration.

The European landscape

France is part of a broader European move toward real-time VAT data.

.webp)

France and Belgium are converging toward a dual e-invoicing and e-reporting model, while Spain illustrates the benefits of near real-time VAT data.

Conclusion: a turning point for POS systems

E-reporting is not just a compliance requirement, it represents a structural shift in how sales data is managed and shared.

POS systems are evolving from simple checkout tools into strategic data hubs, central to tax and financial automation.

Through Chift's unified API, POS providers and financial software publishers can reframe this reform into an opportunity for automation, reliability, and compliance.

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.webp)

.webp)

.webp)

.jpg)

.webp)

.avif)